Stacy’s Savvy Financial Advice

Stay Savvy with our founder Stacy Francis’ latest articles on financial planning, budgeting, debt management, investing, divorce, retirement planning, and more.

Stacy Francis founded Savvy Ladies® in 2003 with the mission to educate women about their finances and empower them to make proactive choices. Inspired by her grandmother who stayed in an abusive relationship due to financial reasons, Stacy has been determined to never let another woman become powerless by financial instability.

Get the resources, knowledge, and tools you need to make smart and informed decisions about your money and your life.

In addition to being the Founder and Board Chair of Savvy Ladies®, Stacy is the President, CEO of Francis Financial, Inc., a boutique wealth management and financial planning firm. A nationally recognized financial expert, she holds a CFP® from the New York University Center for Finance, Law, and Taxation, and is a Certified Divorce Financial Analyst® (CDFA®), a Divorce Financial Strategist™ as well as a Certified Estate & Trust Specialist (CES™).

Stacy has appeared on CNBC, NBC, PBS, CNN, Good Morning America, and many other TV & Financial News outlets. Stacy too is ofter sought out for her advice and can be found quoted in over 100 publications such as Investment News, The New York Times, The Wall Street Journal, USA Today. She shares her wisdom and expert financial advice here for you to learn and get savvy about your finances.

Financial Knowledge is Power. Be Empowered and Find the Advice You Deserve.

Know that Savvy Ladies® is here for you! Should you like to seek advice on a personal financial question, please visit our Free Financial Helpline and get matched with a pro bono financial professional, click here.

STACY’S $AVVY ADVICE

Tax Preparation & Filing Made Simple

by Stacy Francis, CFP®, CDFA

Tax season is here! Time to panic over lost receipts, missing information on cost bases for stocks, and 1099s that won’t ever show up; or, time to spend an afternoon with your CPA; or, click a few buttons on your computer keyboard? It all depends on how organized you’ve been and how well you’ve prepared throughout the year, not just in April. Below are a few tips for how to reduce your tax-related paperwork, now and in the future.

Meet with a CPA. This is by far the easiest way to take the tax filing burden off your shoulders. CPAs file people’s taxes for a living, so you can trust that they know all the tricks and traps. Save yourself time and hassle by asking friends, colleagues or family for a referral.

E-File. If you do not wish to use an accountant, you can find a variety of simple and user-friendly e-filing programs online. Many of them are free, as long as your income is below certain limits. Save yourself some wrestling with your printer and a trip to the post office by filing online.

The Manila Folder. Throughout the year, you will need to save documents such as receipts and transaction reports from your investment accounts. Whenever you receive one of these documents, stick it in a labeled manila folder. If you’re paperless, create a folder on your computer for the same purpose.

Take Advantage of IRA Accounts. Saving in IRA accounts will save you heaps of paperwork, as this eliminates the need to track cost basis and sales price for each security, and include these in your tax report. Once the money is in your traditional IRA or 401(k), it is off your tax record until you start to make withdrawals, at retirement. In case of a Roth IRA, you never have to worry about it again!

Take the Standard Deduction. True, many people save a lot of money by itemizing . . . but it does require both time and effort. If your objective is to keep things simple, take the standard deduction. However, it is usually worth it to itemize. It could save you a lot of money.

Filing your taxes is never fun – unless, of course, you are expecting a huge refund! Use these tricks to simplify your tax filing process and minimize the time you need to spend in your home office, shuffling paperwork.

Should You Do Your Own Taxes?

Here are a few things indicating that you could be better off on your own:

- You know your filing situation (you are up to date with legislation, know your status, etc) and have a very simple financial situation.

- You are organized and have your paperwork ready to go.

- You prefer not to disclose your financials to anyone.

On the other hand, these things may be signs you need help:

- Your financial situation is complex.

- You don’t want to waste time and energy preparing your return.

- Your life has changed drastically, and your filing this year will be very different from last year.

- You want the confidence of working with a trusted advisor.

Should You File Jointly or Separately?

What are the benefits versus drawbacks associated with married couples filing separately? An excellent question. The answer will depend on the circumstances. Below are a few examples of cases where it may be a good idea to keep this one aspect of your life together separate.

- You or your husband has made little money and had lots of medical expenses. By filing separately, the proportions of the two may work out so that you or your hubby can itemize the medical expenses and save well-needed dollars.

- Your partner uses questionable techniques for keeping his tax dollars to himself. While tempting, such actions are illegal, and if you sign the same tax return, you, too, are responsible. If you file separately, your chances of arguing in front of a jury that you didn’t know are much better.

- Your marriage is crumbling. If you are fairly certain that your twosome isn’t going to last, you may want to file separately in order to minimize the paperwork you need to do together later. It is also important to file separately if you are concerned that he is not being 100% honest on his tax reporting.

It is imperative that you stay up to date with the newest rules and limits for the different tax brackets. Taxation is a complicated matter – but you do have options. When you add knowledge to the pot, you can make an informed decision.

Taxes: Quick Tips & Free Resources for Women

One of the best ways to overcome anxiety and experience less stress around taxes is to get informed and ask for help from professionals. Women especially have to be informed because we have special tax issues.

- Women tend to live longer than men.

- Women earn less money compared to men.

- Women hold two times as many single home mortgages as those by men.

- Women-owned business have special tax implications.

With all these issues facing women and their taxes, it is crucial to know where you can get help. The good news is that it’s pretty easy to find help with taxes. Aside from finding your own accountant, you have other options. Some of these options include:

- Savvy Ladies’ Helpline – Submit your question and we’ll put you in touch with a tax expert. It’s confidential and 100% FREE.

- Understanding Taxes – An interactive online tax tutorial by the Internal Revenue Service (IRS). This program is split into two parts: a) the HOWs of taxes and b) the WHYs of taxes.

- Volunteer Income Tax Assistance (VITA) – This program is designed to help those individuals whose incomes are less than $36,000. Another advantage is that VITA has locations in very convenient places such as libraries, schools, shopping malls, community and neighborhood centers, and other locations. You can search for a VITA location near you.

Lastly, keep in mind the following five tips (courtesy SCORE) on how to start tax season by filing taxes correctly:

- Consult an advisor.

- Pay estimated federal and state taxes four times a year.

- Keep good records of both income and expense.

- Ask your tax advisor about special deductions.

- Schedule a tax-tune up at least once a year.

Remember, it’s important you stay ahead of the tax game by being organized and well informed. It will only make your tax season that much easier and (hopefully!) stress-free.

Be Savvy With Your Tax Refund

by Stacy Francis, CFP®, CDFA

One of the only positive aspects of tax season is your refund. A new pair of shoes, dress or a vacation are all tempting choices for us to spend our tax return money. While a small splurge is a must, these extra dollars also give you a chance to improve your finances for the long haul.

One of the only positive aspects of tax season is your refund. We all look forward to a little extra cash. It’s tempting to take that money and splurge – you worked hard for that money, right?

While a small splurge is a must, these extra dollars also give you a chance to improve your finances for the long haul. There are six important areas you can invest the money returned from Uncle Sam that will help you get ahead much more than buying that cute pair of shoes.

1. Pay off credit card debt

Paying just the monthly balance on your credit cards is not a wise way to use credit. Over time the amount you owe will keep accumulating, bringing the original purchases you made to be more than triple the original cost. You do not build any equity by using credit cards. Paying off your debt will strengthen your credit rating, which then leads to a lower interest rate. Pay off the cards with the highest rates first. Read more about credit card debt.

2. Open an Individual Retirement Account (IRA)*

The greatest advantage to opening an IRA is that you earn tax-free interest: use your money to make more money. IRAs help you gain tax advantages to your investing and can be opened for free. They are great retirement saving tools. Any payments you have made before April 15th give you an entire year’s start.

A Traditional IRA is different from a Roth IRA. No taxes are paid while the money is invested in a traditional IRA until you begin withdrawing money during retirement. Here’s a chart from TRowe Price to understand the differences.

Opening an IRA for a child is the perfect gift because it gives the money a long time to grow and is an excellent example of the power of starting early and compounding interest.

*Do you have an employer sponsored retirement plan: 401(k) or 403(b)? Make sure you are contributing the maximum amount allowed, especially if your employer is matching your contributions. Read more about retirement planning.

3. Start or contribute to an Emergency Fund

Financial experts suggest saving between 6-8 months of your monthly expenses in case of an emergency. Think about opening an online savings account. You’ll earn more money by receiving higher interest rates than going to a traditional “brick and mortar” bank. You receive 24-hour access to your funds and it takes about five minutes to open an account. Read more about the importance of an emergency fund.

4. Pay down some of the principal on your mortgage

Your home mortgage provides a return on investment more reliable than anything the stock market can offer. Yet more than half of your monthly mortgage goes directly into the bank’s pocket; i.e., interest payments. If you pay more than your monthly payments it’s applied directly to your mortgage’s principal balance. Hence, you save a lot of time off your mortgage; i.e., reduce total interest paid. Use this calculator to determine what you will save and gift yourself the peace of mind in knowing you own your home.

5. Invest in yourself

Your biggest asset is not your bank account balance, it is actually your earning capacity. Spend your money on continuing education classes that will increase your marketability, promotion chances and employment value. You could also start your own business to bring in extra income over time.

Consider these five ways to spend your tax refund and you will have greater financial security now and beyond.

Reduce or eliminate a refund for next year

Yes, it’s fun to get a refund. However, if you’re getting a large refund, you’ve given the Internal Revenue Service an interest-free loan of your money for the previous year. What should you do to avoid giving the IRS another interest-free loan this year? You may need to increase the number of allowances claimed on your Form W-4 or reduce your estimated tax payments. Or both. But don’t get carried away. Big underpayments will result in a nasty tax bill next year. How much should you withhold?

Get that refund working for you!

Top 6 Tips for Improving Your Credit Score

By Stacy Francis, CFP®, CDFA

According to myFICO, it’s important to note that repairing bad credit is a bit like losing weight: It takes time, and there is no quick fix. In fact, out of all of the ways to improve a credit score, quick-fix efforts are the most likely to backfire, so beware of any advice that claims to improve your credit score fast.

Here are some of the top tips to raise your score.

- Pay down balances and pay off all outstanding debts. A main ingredient in the credit score formula, the size of your balances really does matter. Pay them down – or even better, off. Here’s more advice on paying off credit card debt.

- Protest unfair information. If you have an entry on your credit report that shouldn’t be there (honestly, now), know that you can dispute it. If you submit complaints to the company that posted it as well as the credit-reporting agency, they will investigate and take it off, leaving your record a whole lot cleaner.

- Contact creditors. Write letters to creditors explaining any payments that were more than 60 days late. Request that the creditor share that information with the credit companies. If you’ve been a loyal customer for years and normally make your payments on time, chances are, if you talk to customer service, they will disregard that one time you forgot to pay your bill because you were on your honeymoon. Ask politely – and thou shall receive.

- Don’t neglect the oldies. Another important factor in the credit score formula is how long your accounts have been open. So even if the Victoria’s Secret card you applied for when you were in college doesn’t have the most useful perks, use it once in a while for a credit score boost.

- Cancel any credit cards or department store cards that you don’t use. Be sure to put the cancellation in writing so the account will show you canceled it versus the credit card company.

- Pay your bills on time. It seems simple, yet so many people fail on this count. If you have a hard time remembering your payments, set up a reminder.

Be careful about tainting your good credit with debt incurred by someone else with lower credit quality than you, such as a new spouse. Help your partner clean up his or her credit before you begin co-signing on additional credit.

Removing Incorrect Entries from your Credit Report

Many people don’t know that if you feel an entry on your credit report has been put there in error, you can complain in writing to the credit-reporting agency (meaning that if this certain record has been reported to all three agencies, you need to send letters to each one of them separately). The agency then advises the company that put the entry on your record about your complaint, and it has thirty days to respond and strengthen its case. If it fails to do so, the reporting agency removes the entry from your record.

This may sound like a “so what?”, but the truth is many companies are so overwhelmed, if your entry is minor enough (or complicated enough), chances are, they won’t think it’s worth their time to fight your claim. I know many people who have used this technique to improve their credit histories – and thus their futures. It only takes a few letters, and the most it’ll cost you is a couple of stamps.

So next time the thought of spending hours on the phone trying to cut through layers of bureaucracy makes you cringe, try this alternative approach and throw the bureaucracy right back at them!

READ ALSO: What You Need to Know About Credit

Do you have any financial questions? Contact the Savvy Ladies Free Financial Helpline today and get free mentoring from a financial advisor.

What You Need to Know About Credit

By Stacy Francis, CFP®, CDFA

You sit down in your mortgage broker’s office because you can’t stand the news. Your credit is so bad you will not be able to secure a loan to buy the dream home you just bid on. Can you imagine? After months of taking time off work to run from one open house to the next, you forgot to check your credit report to make sure your credit was in order. What independent credit reporting agencies say about you and your credit can and will make the difference between your ability to buy a car, a house, or even a simple pair of shoes.

Your credit report contains everything about your credit history, including the good, the bad, and the ugly. Details you would never dream of sharing with even your closest of friends are listed neatly for all creditors to see. Your last residence, your employment history, your bill payment history, how many credit cards you have, how much you owe, and how much access to credit you already have are just a few of the juicy details contained within your report.

How Your Credit Score Affects Your Finances

Every time you apply for a new card, your credit score goes down. This can affect your finances in many more ways than you would think. Below are just a few.

- The lower your credit score, the more expensive it is to finance anything – from your dream home to that sweet new car. When you have a low credit score, banks and similar institutions consider you a high-risk individual, so if you want a mortgage, be prepared to pay for it.

- A low credit score can make it expensive at best, impossible at worst, for you to get a loan, should disaster strike.

- It might make it harder to lease a place. Many landlords will only lease their apartments or houses to people in good to excellent credit standing.

- You may need to put down a deposit – lock your money up without earning any interest – even for things as ordinary as, say, cell phone service.

- Your credit score may cost you that job you want — most notably any type of position where you work with money, be it in a bank or another type of financial institution.

So what hurts your credit?

Paying bills late, defaults on loans, too many credit cards, canceling your credit cards, large balances, medical bills that were lost in an insurance shuffle can all end up creating black marks on your credit report.

Many major life events, such as marriage and divorce, purchasing a home, or having a child are also financial changes that involve and can affect your credit.

Many credit files contain inaccuracies that can harm your credit rating. Just as reviewing your credit card statement can reveal charges you did not make, reviewing your credit report can reveal activity on accounts you don’t use or new accounts you did not open, alerting you to the possibility of identity theft.

FICO 8: Credit Scoring System

Even the most responsible borrowers slip up sometimes. Maybe a utility bill went unpaid after you moved and the missed payment went into collections. Or perhaps there are unpaid library fines or parking tickets in collections that are hanging on to your credit history and affecting your FICO credit score, which is widely used by lenders to evaluate your ability to repay debt.

With the newest version of the FICO credit scoring system, however, minor delinquencies are now overlooked in calculating credit worthiness.

Under the updated scoring model, called FICO 8, small missed payments lingering in collections with original amounts of $100 or less will no longer do damage to your credit score.

Consumers also are less likely to be penalized for any single delinquency if it occurred two or more years ago- and if their credit history is otherwise unblemished. There’s more flexibility with missing a payment. If you have a more habitual pattern of paying accounts late, you’re more likely to get penalized for that.

If a consumer’s credit usage is high, that will be more likely to hurt his or her score with FICO 8. But getting close to your credit card limits- even if you always pay on time- is penalized in some way in every FICO score, not only the recent edition.

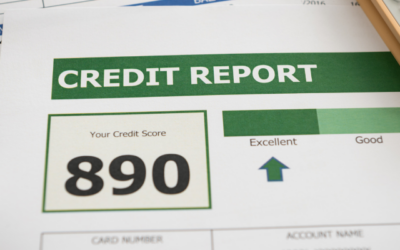

Finding and Understanding Your Credit Score

There are three major credit-reporting agencies: Experian, Equifax, and TransUnion. The information on their reports tends to vary slightly. You can get your credit report for free from www.annualcreditreport.com

Once you have your reports, you should check them for accuracy. If you see anything that shouldn’t be there, make sure you contact the reporting agency/agencies to dispute it.

Looking at your reports for the first time can be something of a cold shower, as they will list every single late payment you have ever made in your life, as well as how late it was.

The actual score is a snapshot of your creditworthiness at any given time. It is calculated by a machine, and influenced by many factors such as available credit, outstanding debt, length of credit history, and late payments. As these variables vary, so does your score. So the good news is that when you clean up your report, make your payments on time, and reduce your outstanding debt, over time your credit score will be better and better.

Correcting Mistakes in Your Credit Report

Few Savvy Ladies know that they can fight an improper charge on their credit card. The Fair Credit Billing Act, which was passed in 1974, makes sure the law is on your side. In fact, your credit card company is required to investigate and either correct the mistake or explain why the bill is correct within 90 days. They must acknowledge your complaint within 30 days.

Make sure to put your complaint in writing and send it via certified mail to “Billing Inquiries,” which is listed on the back of your card statement. According to the law, your dispute letter must include your name, address, account number and a description of the problem. Visit Bankrate.com for a sample dispute letter to help you on your way. The deadline for notifying your credit card company of a billing error is 60 days from the date the bill was mailed to you. Keep in mind that the 60-day clock starts ticking on the day your issuer mails your billing statement, not the date you receive it. So by the time you receive your bill, you actually have 50-odd days to get a dispute letter back to your card issuer.

Request your free credit report online or by calling 1-877-322-8228. You can also contact any of the following “big three” credit reporting agencies: Equifax, Experian, or TransUnion.

Different Types of Debt: Which Should I Pay Off First?

By Stacy Francis, CFP®, CDFA

At a recent get-together at my parents house, one of their friends was excited to tell me his company had given him a substantial bonus – one that far exceeded his expectations. Thrilled to have a financial expert at the party, he asked whether I thought he should invest the money, or use it to pay down debt.

This is a brilliant question, and one that is fairly simple to answer. It depends on the cost of your debt, as well as the return on the investment you are considering. Some types of debt, like credit card debt, are expensive, so if you have them you should definitely use the money to pay them off. I know it sounds boring, but you will be happy later, when financing charges stop eating half your paycheck.

Other types of debt, such as student loans and mortgages, tend to have fairly reasonable rates and long payback times. Hence, you may be better off investing the money than paying them off. Say, for instance, that you pay 6% interest on your mortgage, and the yield from the investment you would like to try is 8%. In this case, depending on what kind of risk comes with the potential investment, you may be able to walk away with an extra 2% per year if you invest the money rather than dumping it into your home.

As all the debt my parents’ friend had was a low-interest mortgage, he decided to invest the money – after treating himself to a cruise with his wife. After all, life’s supposed to be lived. As for you, next time you come across a larger-than-expected sum of money, compare rates. The answer to this question is simply mathematical.

Types of Debt, From Worst to Best

My parents’ friend is far from the only one having a hard time keeping different types of debt apart. With this in mind, here’s a list of different types of debt, starting with the kinds you want to lose right away and ending with the types you may actually want to keep.

- Credit card debt. Don’t do it, and if you have already done it, pay it back and never do it again. It’s that simple.

- Loans against your 401(k). These are nowhere near as bad as credit card debt, but losing them will enhance your financial health significantly.

- Auto loans. As long as you can afford your monthly payment without any problems, you can keep this type of debt.

- Home equity loans/second mortgages. This loan type should be paid off before you consider losing the categories below.

- Student debt. Student loans tend to be pretty favorable – pay them off after the types above, but before you consider making a dent in your mortgage.

- Mortgages. Interest rates are generally favorable for mortgages, making it more important to contribute to 401(k) plans and other types of retirement savings accounts than paying off your mortgage.

How Much Debt is Too Much?

Debt is truly a widespread problem these days. So with each of my clients who are trying to regain control of their money, I usually start out by breaking down their finances – income, costs, spending, and debt. In many cases, their debt-to-income ratio comes out higher than the limits most lending institutions use when determining how large a mortgage an individual can carry. According to them, if your debt payments (including mortgage payments) eat up more than 36% of your gross income, you should consider changing your lifestyle. If you do not own a home, of course your debt payments should be much smaller than that. Still, many people are far deeper in debt.

The good news is, by taking an honest look at your finances, drafting a budget, and making changes – some smaller, some bigger – you can turn this around and face a brighter financial future. I see it happen all the time. All you need is determination and a network of people who support you.

Take debt management courses (and other financial literacy classes) for free! Sign up for the Savvy Ladies Financial Knowledge Program here.

Use Affirmations to Attract More Money!

by Stacy Francis, CFP®, CDFA

14 Money Affirmation tips from Stacy Francis, Founder Savvy Ladies

So you desire to have a more rich and rewarding life? One of the most effective ways to do this is by harnessing the life-changing power of prosperity affirmations. When you are emotionally connected to your desire for more wealth and happiness you can use the power of affirmations to see how quickly your need is manifested!

Affirmations are very powerful tools for transformation and self-empowerment. If you intend to bring anything new and positive into your life, monitoring and control of your thoughts and words are very important.

Use of your daily financial affirmations will help you to be more loving and positive toward yourself and others at all times, in every situation. Listen to your heart, and know that as you learn and grow, you will not only transform yourself in a positive way but will attract prosperity into your life!

Use the following power prosperity affirmation for attracting money.

Prosperity Financial Affirmation: Money comes to me easily and effortlessly.

Tips on Using Prosperity Financial Affirmations

- Give up all negative talk about yourself or any others. If the dialogue is internal, use your affirmation. If it is from an external source, say something positive, or simply smile and walk away from the conversation.

- Stay in the now. Forget the past. Forget the future. They don’t exist.

- Repeat the affirmation out loud and/or to yourself as often as possible throughout the day.

- Sing the affirmation – in the shower, in the bath, in your car, to your children.

- Write it out 50 or 100 times – whatever you have time for.

- Get some post-it notes and stick them on your computer as you work. Better yet, change your screen-saver every day!

- Place it on your bathroom mirror.

- Place it in your wallet or in your purse.

- Place it beside you as you drive your car.

- Keep the radio off and repeat the affirmation on your way to and from work.

- Record it on a tape and play it in your vehicle as you drive.

- Create a large corkboard and get some thumbtacks and plenty of sheets of colored paper. Each day, write your affirmation down on the paper and tack it to your corkboard. Make it interesting by cutting out different shapes – like hearts or diamonds or spirals, or even ladders with rungs… Very soon, you will have a rainbow of colors and shapes on your corkboard, filled with colorful, positive affirmations.

- Journal your affirmations. Write down your experiences. Write down your dreams. Share them with others who are doing this with you.

- Stay positive!

Originally published April 25th, 2014

Fixed vs. Variable Expenses: What’s the Difference?

by Stacy Francis, CFP®, CDFA, Founder Savvy Ladies

Perusing the annual report of a company that I am invested in, I got to thinking about how these two words are so much more than just accounting jargon. They affect your financial future to a much greater extent than you may think. So let’s break them down and look at what fixed and variable expenses are – and aren’t.

What Are Fixed Expenses?

Fixed expenses are all reoccurring expenses – from rent or mortgage bills to car payments as well as tuition or childcare expenses for your children. Other bills that fall under this category include health insurance, life insurance, and essential utilities. We typically do not pay much attention to these costs, but most of our budget goes toward funding them.

These fixed expenses occur repeatedly and typically can’t be dropped with a moment’s notice, should your financial situation change. Therefore, it is essential to make sure that your fixed expenses are as low as possible, allowing you ample funds for variable costs that are often harder to control and savings. Fixed costs should take up no more than 50% of your income to make sure that you have enough breathing room in your cashflow.

Examples of Fixed Expenses:

- Rent

- Mortgage

- Health insurance

- Life insurance

- Car loan payments

- Tuition

- Childcare expenses

- Essential utilities

What Are Variable Expenses?

Classic examples of variable expenses are clothing, vacations, entertainment, eating out, gifts, facials, and home goods.

Many variable expenses happen sporadically only a few times a year. Think of that plane ticket you just booked to see your family in California. However, some variable costs happen every month. For example, gas, parking fees, groceries, and personal care expenses in any given month could be different from previous payments or ones you’ll make in the future.

Sporadic and ongoing variable costs can make budgeting very difficult because you never really know how much you need for this part of your monthly spending.

That being said, variable costs that can change from month to month should take up no more than 30% of your income. The positive about many of your variable expenses is that you usually have a little more control over them, and you can drop many of them if you really needed to. In addition, variable expenses are generally much easier to lower than fixed expenses like your housing.

Examples of Variable Expenses:

- Groceries

- Gas

- Clothing

- Personal care expenses

- Home goods

- Vacations

- Entertainment

- Eating out

- Parking fees

- Gifts

Savings Expenses

You might not have ever thought about savings as a monthly expense, but you should! Your goal should be to saving 20% of your income for the future. These dollars can be stashed into an emergency fund, invested in retirement, or used to kickstart your down payment savings for your first home.

If you are like most people, you struggle to save for short-term and long-term goals. According to Bankrate, one in five American adults do not save at all. Just 16 percent of those surveyed report socking away more than 15% of their income. When Bankrate asked their survey participants why they missed the mark, the top reason given was expenses. Is this the case for you too?

Fixed vs. Variable Expenses: Considerations for Your Budget

If you could use more breathing room in your budget, you should review your fixes and variable expenses, keeping the 50/30/20 rule in mind.

The 50/20/30 rule

- Fixed costs that stay the same month after month, such as your rent or mortgage, car payment, and cable bill, should take up 50% of your income.

- Variable costs that can change from month to month, such as entertainment, groceries, and clothing, should take up 30% of your income.

- Savings should take up 20% of your income.

Reviewing your fixed expenses will significantly impact how much you can save each month because they make up most of your spending. However, the negative is that reductions can be more brutal to come by and might require a change in the home you rent or own and the car you drive. More manageable fixed expenses that you can reduce can be had by changing cell phone plans, canceling extra cable channels, shopping for less expensive insurance, or refinancing your home for a lower mortgage interest rate.

The upside of having variable expenses in your budget is that you have more control over them than you do with fixed payments. It is typically easier to find opportunities to save money, but you need to think about this spending every day. If you want to save money on variable expenses, it may require some lifestyle adjustments. For example, cutting back or cutting out things like dinners or new clothes are simple ways to save. You could also save on groceries and dining out by planning meals, using coupons, or switching from name brands to generic.

Everyone deserves to splurge from time to time. But when you do – make sure you keep the 50/30/20 rule in mind. Keeping your expenses down is one of the critical factors in the quest for financial independence.

Looking to get on top of your finances? Download our free budgeting worksheet here.

Investing in uncertain times – using stocks and bonds to secure your financial future

In this webinar, Stacy Francis, CFP®, CDFA®, CES™ discusses how to create financial immunity and protect your portfolio during market volatility. In her presentation, you will also learn what moves you can make to stay on the right track with your investments and retirement, and discover how you can be financially resilient in these times of uncertainty.

About Stacy:

Stacy Francis is the President and CEO of Francis Financial, Inc., a fee-only boutique Wealth Management, Financial Planning and Divorce Financial Planning firm dedicated to providing ongoing comprehensive advice for successful individuals, couples and women in transition such as divorce or widowhood. Stacy has over 20 years of experience in the financial industry. She attended the New York University Center for Finance, Law and Taxation, where she completed the Certified Financial Planner™ (CFP®) designation. Stacy is also a Certified Divorce Financial Analyst® (CDFA®) as well as a Certified Estate and Trust Specialist (CES™). Stacy has mastered specialized training in the financial issues of divorce and is the Director of the Association of Divorce Financial Planners (ADFP) Greater New York Metro Chapter.

Stacy is the founder of Savvy Ladies™, a nonprofit organization dedicated to educating and empowering women to take control of their finances. Savvy Ladies has helped over 20,000 women through free one-on-one financial counseling, workshops and retreats. Stacy also gives back as a board member of FamilyKind, a nonprofit organization offering NYC divorce services to adults and children experiencing separation or divorce.

She is a nationally-recognized financial expert being one of twenty of the nation’s leading wealth managers on CNBC’s Digital Financial Advisor Council, a member of the Forbes Finance Council as well as an expert contributor for The Wall Street Journal. Stacy’s expertise is highlighted in over 200 media publications, articles, bylined pieces and quotes. Stacy is the host of Financially Ever After, a podcast focusing on women, money and divorce. She is also the author of the white paper, Unveiling the Unspoken Truth: The Financial Challenges Women Face During and After Divorce.

Stacy has received numerous industry awards, among them, Investopedia 100 Top Financial Advisors, Investment News Women to Watch, Financial Planning Association’s Heart of Financial Planning Award, Financial Planning Magazine’s Pro Bono Award and the NAPFA Consumer Education Foundation’s first Pro Bono Award. She was also listed as a national Money Hero by CNN Money Magazine, one of the Top Wealth Advisor Moms by Working Mother Magazine and one of the best financial Advisors for women by the Women’s Choice Award. The firm has been named one of the Top 10 Best Financial Advisors in New York for 4 years in a row.

How the CARES Act Affects Your Small Business

Join us for this special conversation with Savvy Ladies Founder, Stacy Francis, CFP®, CDFA®, CES™.

Stacy will discuss how the CARES Act affects your small business. You’ll learn about the benefits, eligibility, and the application process.

About Stacy:

Stacy Francis is the President and CEO of Francis Financial, Inc., a fee-only boutique wealth management, financial planning and divorce financial planning firm dedicated to providing ongoing comprehensive advice for successful individuals, couples and women in transition such as divorce or widowhood. Stacy has over 20 years of experience in the financial industry. She attended the New York University Center for Finance, Law and Taxation, where she completed the Certified Financial Planner™ (CFP®) designation. Stacy is also a Certified Divorce Financial Analyst® (CDFA®) as well as a Certified Estate and Trust Specialist (CES™).

Stacy is the founder of Savvy Ladies™, a nonprofit organization dedicated to educating and empowering women and that has helped over 15,000 women make proactive choices about their finances. She is a nationally-recognized financial expert being one of twenty of the nation’s leading wealth managers on CNBC’s Digital Financial Advisor Council, a member of the Forbes Finance Council as well as an expert contributor for The Wall Street Journal. Stacy is the host of Financially Ever After, a podcast focusing on women, money and divorce.

Stacy has received numerous industry awards, among them, Investopedia 100 Top Financial Advisors, Investment News Women to Watch, Financial Planning Association’s Heart of Financial Planning Award, Financial Planning Magazine’s Pro Bono Award and the NAPFA Consumer Education Foundation’s first Pro Bono Award. She was also listed as a national Money Hero by CNN Money Magazine, one of the Top Wealth Advisor Moms by Working Mother Magazine and one of the best financial advisors for women by the Women’s Choice Award.